All Categories

Featured

Table of Contents

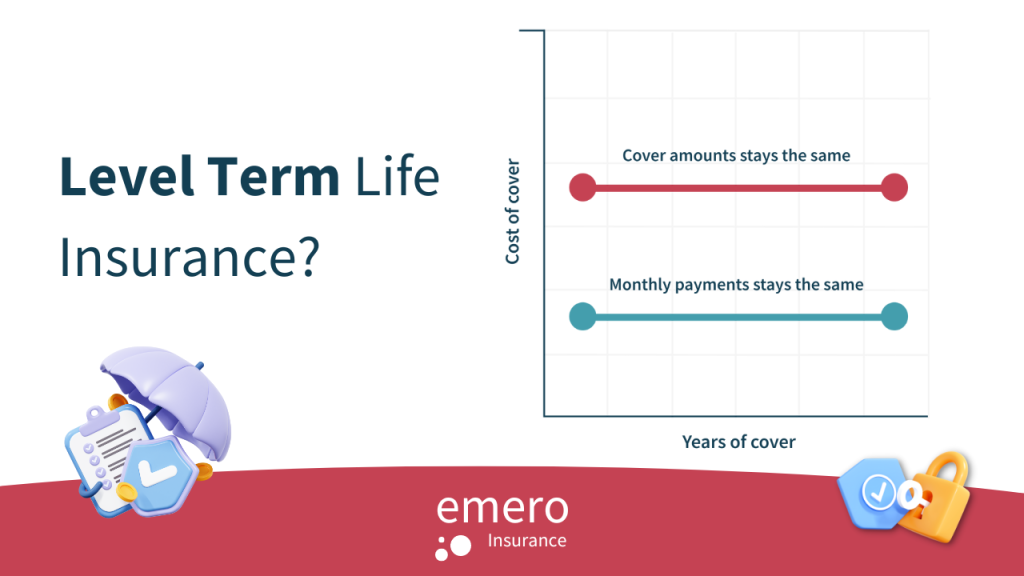

If you select level term life insurance policy, you can allocate your premiums since they'll remain the exact same throughout your term (Level term life insurance). Plus, you'll know specifically how much of a survivor benefit your beneficiaries will obtain if you die, as this quantity won't transform either. The rates for degree term life insurance policy will certainly depend on several variables, like your age, wellness status, and the insurance provider you pick

As soon as you experience the application and medical examination, the life insurance policy business will certainly review your application. They should educate you of whether you've been approved shortly after you use. Upon authorization, you can pay your very first premium and authorize any relevant paperwork to guarantee you're covered. From there, you'll pay your costs on a month-to-month or annual basis.

You can pick a 10, 20, or 30 year term and take pleasure in the included tranquility of mind you should have. Working with a representative can help you discover a policy that functions ideal for your needs.

This is regardless of whether the insured individual passes away on the day the policy starts or the day before the plan finishes. A degree term life insurance policy can suit a wide array of situations and demands.

What are the top Best Level Term Life Insurance providers in my area?

Your life insurance policy policy might also create part of your estate, so can be subject to Inheritance Tax learnt more regarding life insurance policy and tax. Let's take a look at some attributes of Life Insurance policy from Legal & General: Minimum age 18 Optimum age 77 (Life Insurance), or 67 (with Essential Health Problem Cover).

The amount you pay remains the same, yet the level of cover reduces approximately in line with the way a payment home mortgage reduces. Lowering life insurance coverage can help your liked ones stay in the household home and prevent any further interruption if you were to pass away.

Term life insurance coverage provides coverage for a particular period of time, or "term" of years. If the insured individual passes away within the "term" of the plan and the plan is still effective (active), then the fatality benefit is paid to the recipient. This sort of insurance policy normally enables customers to initially buy even more insurance policy protection for much less money (premium) than other kinds of life insurance.

Tax Benefits Of Level Term Life Insurance

If any individual is depending upon your earnings or if you have commitments (debt, home loan, etc) that would certainly drop to somebody else to take care of if you were to pass away, then the answer is, "Yes." Life insurance serves as a replacement for earnings. Have you ever before computed just how much you'll make in your lifetime? Normally, throughout your functioning years, the answer is usually "a ton of money." The prospective danger of shedding that making power incomes you'll require to money your family members's most significant goals like purchasing a home, paying for your kids' education and learning, lowering financial obligation, saving for retirement, etc.

One of the major appeals of term life insurance policy is that you can get even more insurance coverage for much less cash. However, the protection expires at the end of the policy's term. One more means term policies differ from whole life or permanent insurance is that they normally do not develop cash money worth in time.

The theory behind reducing the payout later on in life is that the insured prepares for having reduced protection requirements. You (ideally) will owe less on your home loan and other debts at age 50 than you would certainly at age 30. As a result, you might choose to pay a reduced premium and lower the amount your beneficiary would certainly obtain, due to the fact that they would not have as much debt to pay on your behalf.

What should I look for in a 30-year Level Term Life Insurance plan?

Our policies are developed to fill out the voids left by SGLI and VGLI strategies. AAFMAA functions to comprehend and support your unique financial goals at every phase of life, customizing our solution to your distinct scenario. online or over the phone with one of our army life insurance coverage experts at and discover more concerning your military and today.

With this kind of protection, premiums are thus ensured to remain the same throughout the contract., the amount of coverage supplied boosts over time.

Term policies are likewise commonly level-premium, however the excess quantity will continue to be the same and not expand. One of the most typical terms are 10, 15, 20, and 30 years, based on the requirements of the insurance policy holder. Level-premium insurance is a kind of life insurance policy in which premiums remain the exact same rate throughout the term, while the quantity of insurance coverage supplied increases.

For a term plan, this means for the size of the term (e.g. 20 or 30 years); and for a permanent policy, till the insured dies. Level-premium plans will usually set you back more up front than annually-renewing life insurance policy plans with regards to just one year at a time. Yet over the future, level-premium payments are usually more economical.

What is Level Term Life Insurance For Families?

They each look for a 30-year term with $1 million in coverage. Jen purchases a guaranteed level-premium plan at around $42 per month, with a 30-year horizon, for a total of $500 per year. But Beth numbers she may just need a plan for three-to-five years or till complete payment of her present financial debts.

In year 1, she pays $240 per year, 1 and around $500 by year 5. In years two through 5, Jen remains to pay $500 per month, and Beth has actually paid an average of simply $357 per year for the same $1 million of protection. If Beth no more requires life insurance coverage at year five, she will have saved a great deal of cash about what Jen paid.

Yearly as Beth grows older, she encounters ever-higher annual premiums. Jen will proceed to pay $500 per year. Life insurance firms are able to provide level-premium plans by basically "over-charging" for the earlier years of the policy, accumulating greater than what is required actuarially to cover the danger of the insured dying during that early period.

1 Life Insurance Policy Statistics, Data And Market Trends 2024. 2 Expense of insurance coverage prices are determined utilizing approaches that differ by company. These prices can differ and will normally raise with age. Rates for active employees might be various than those offered to terminated or retired workers. It is necessary to look at all elements when assessing the overall competition of prices and the value of life insurance protection.

What is included in Low Cost Level Term Life Insurance coverage?

Like the majority of team insurance policies, insurance coverage policies offered by MetLife consist of specific exclusions, exemptions, waiting durations, reductions, limitations and terms for keeping them in pressure. Please call your benefits manager or MetLife for prices and total details.

{kind=link}

Table of Contents

Latest Posts

Seniors Funeral Cover

Funeral Insurance Expenses

Instant Term Life Insurance

More

Latest Posts

Seniors Funeral Cover

Funeral Insurance Expenses

Instant Term Life Insurance